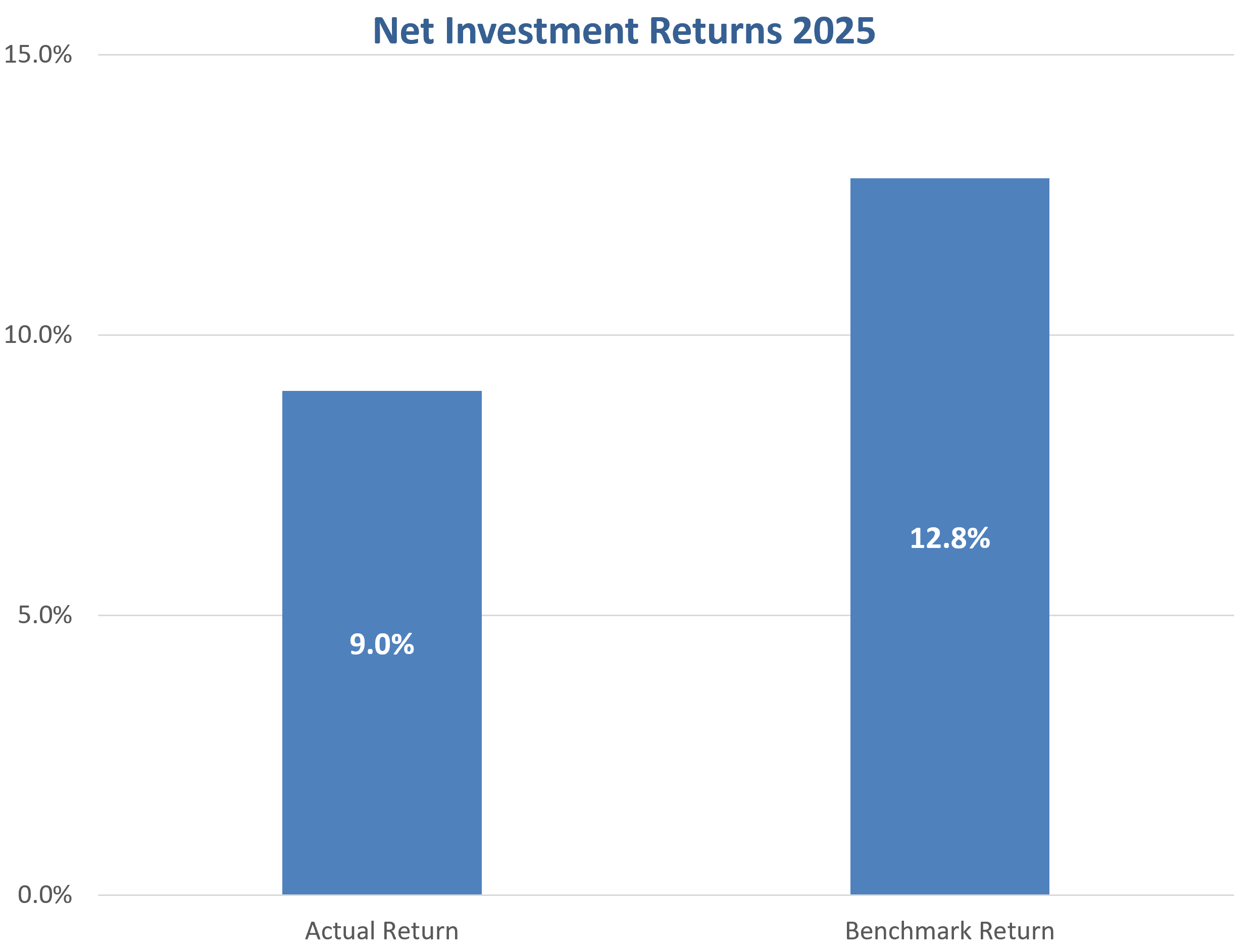

Net Investment Return - 2025

2025 was another year with exceptional performance in public markets. While we generated another strong year of performance, we trailed our benchmark by 3.8% due to shortfalls in the performance of our Real Assets and Private Equity.

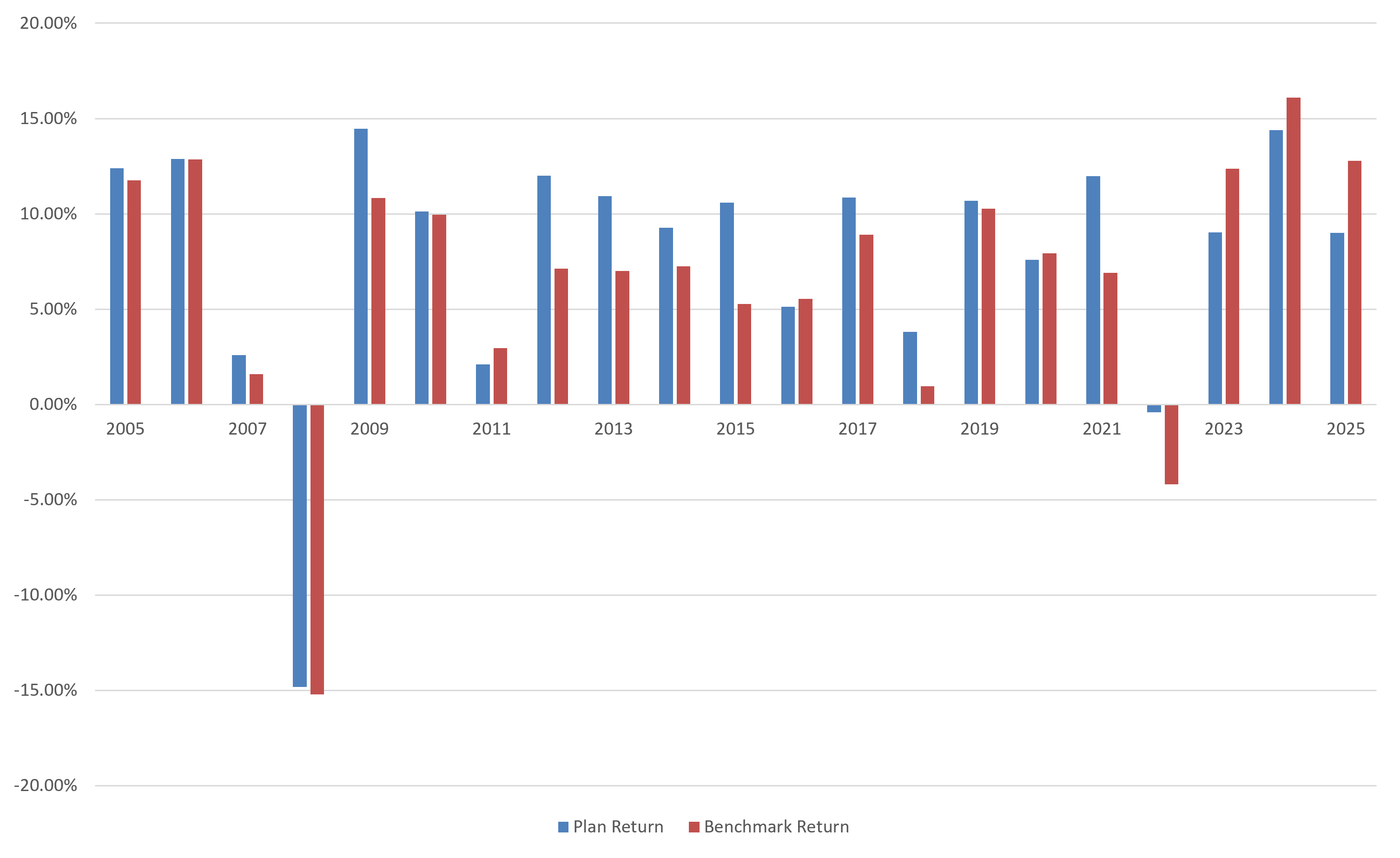

Long-Term Performance

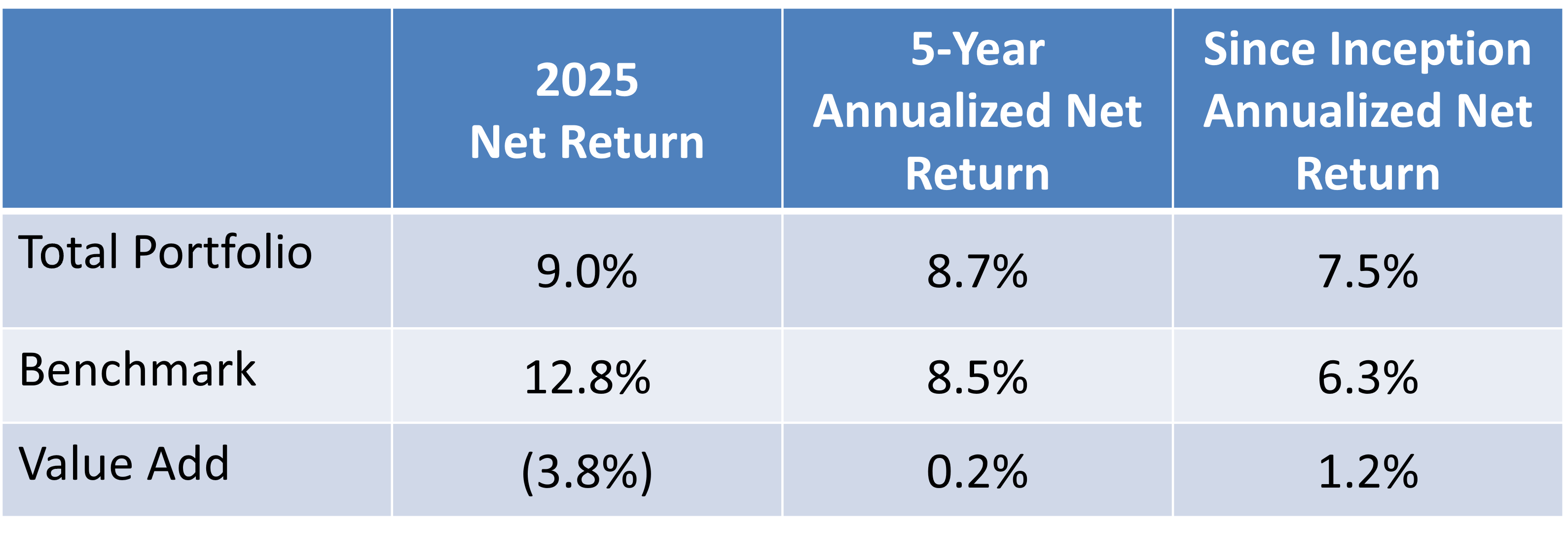

Since pension plans invest for the long-term, it is important to consider our asset performance over an extended period of time. Since inception, our Plan’s assets have generated a net rate of return to 7.5%, benchmark to 6.3% and outperformance to 1.2%. This represents the value-add from our bias towards active investment.

Breaking our returns down into the various sub-portfolios allows us to determine which asset classes are performing well relative to our expectations. Although it may seem appealing to invest a large portion of a portfolio in a single asset class based on historical performance, it is important to note that doing so can add undue risk and compromise long-term sustainability.

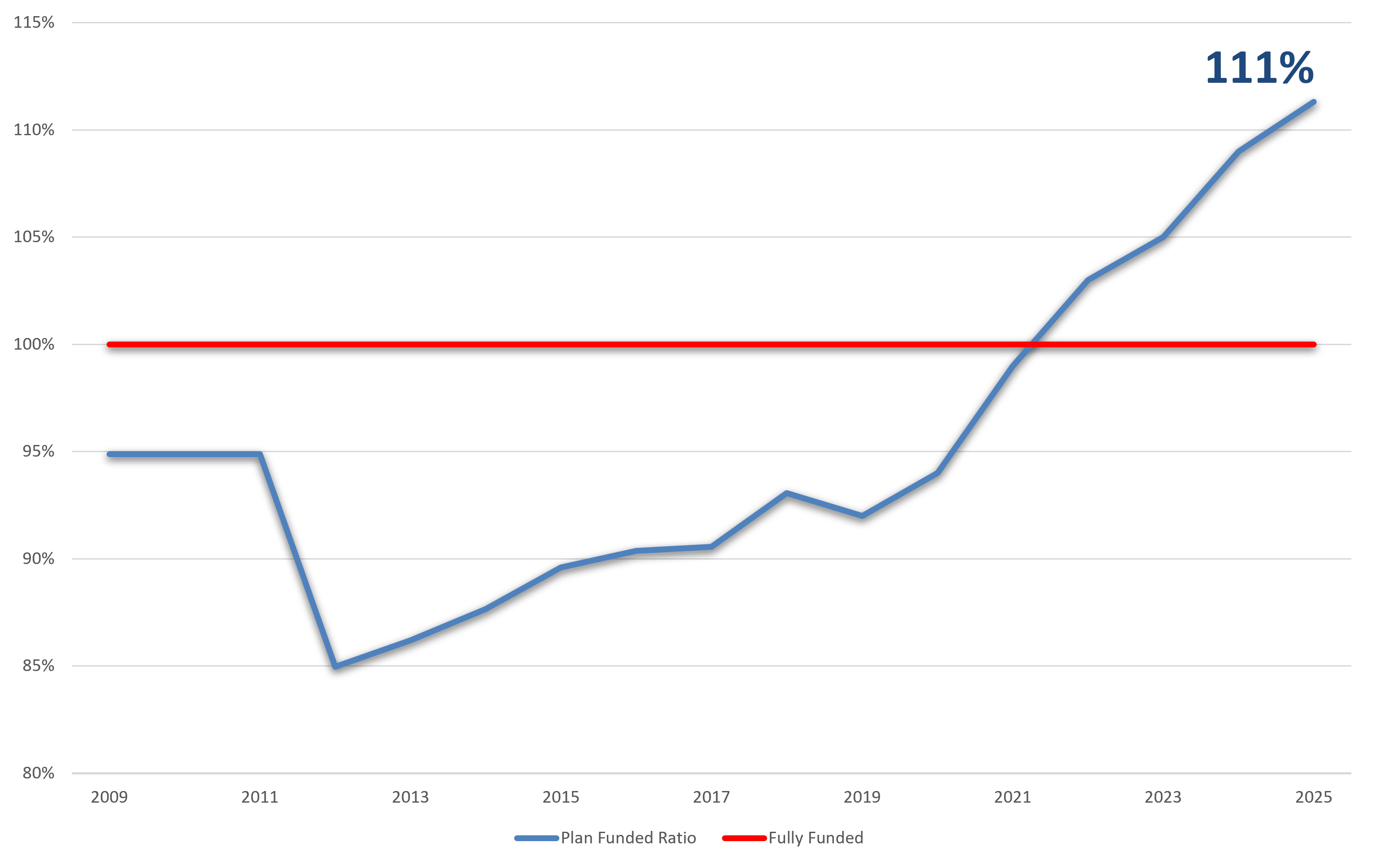

Going Concern Funded Ratio

The Plan is currently estimated to be 111% funded. The Plan's funded ratio is a measure of its financial health and is a key driver of the level of contributions that are required to go into the Plan. It is determined by dividing the Plan's assets by its liabilities. Special contributions, over and above the cost of annual benefit accruals, are being made to bring the Plan to a more sustainable position.